Everyone wants and needs to save money. But how do you make it easier to do so? There are countless traditional methods, but finance technology – FinTech, if you will – is red hot, and finding good traction with well designed, secure apps like Acorns and Digit leading the way. The savings and financial app world still has plenty of needs and room to grow, though.

Enter Milwaukee-based startup Milo, wanting to make change happen with its soon to be released app.

I caught up with one of the co-founders, Craig Sweeney, recently and asked several questions about Milo. Here's what we learned:

OnMilwaukee: Give me the genesis of Milo, please. How did you come up with the idea?

Craig Sweeney: Tom Wondra (one of Milo’s co-founders) and I both have dealt with the high cost of college education – both ourselves and as parents of college-age kids – and wanted to do something to help alleviate that burden. We initially just looked at that from the debt perspective – helping people pay back student loans – but then pivoted the idea to helping parents and teens save for school. I had seen various round-up promotions some banks have used and realized that the mechanics of the round-up are such an amazing way for people to save really easily for their goals – whether it’s for college or other life goals – and quite literally "Make Change Happen" (Milo’s tag line).

What’s your background, and what drew you to this opportunity?

My background is really at the intersection of technology and advertising/marketing, having led business development for a few software startups in the market research space and then as consultant for ad agencies and startups, focusing on growth strategy and tactics. Tom and I met while working together for a digital patient acquisition startup in the pharma space.

I really like the idea of being able to help families – many of them living paycheck to paycheck and not being able to regularly put aside money for important life goals – save "in the background" of their everyday lives. The round-ups add up quite a bit over time. The amounts of the round-ups may not seem like a lot on their own, but over time, with the power of compound interest, Milo can really make a positive impact on people’s lives.

What’s the timeframe for launch?

Milo is in private beta right now, which basically means that we’ve got a small number of users – founders, family, friends mainly – saving with Milo and testing all aspects of the application prior to our general release, which is coming in November of this year.

Financial tech is hot area, for sure, but one with great competition. How does Milo plan to stand out and grow downloads, use and community?

It certainly is a hot area. FinTech was really ripe for disruption. A big part of that is due to consumers distrust – and distaste – for the big banks, especially in light of what happened in 2008 and continues to happen today, with the recent news about Wells Fargo, for instance. A large majority of the startups in the space are really looking to engage with the millennial group exclusively.

While that makes sense, as that’s a large group to be sure, Milo’s research has found that there are other demographic groups that span all life stages that have financial goals they need to put aside for: parents with young children, gen-xers needing to save for retirement, people saving for a wedding or even for a vacation they’ve not been able to take.

Milo’s focus is on our users’ ability to save for their goals thru round-ups, but we really stand out as we are building Milo’s community via our engagement with school districts and our Milo Marketplace, a geo-fenced local community of merchants and retailers which will offer Milo users rewards for their patronage, such as matching their round-ups, special Milo deals, etc. We’ve really received incredible feedback and support from school districts in Southeast Wisconsin as saving with Milo can really make an impact on the financial lives of the families within the districts.

Working with the districts here in Wisconsin – and then nationwide – to promote Milo to the families in their districts is one of two main ways we will be looking for user engagement we feel strongly about. We are also offering Milo as a platform to businesses as an employee benefit to their employee base. We were actually approached by a few employers during our research phase specifically asking for this as a way to bring a low-cost/high-impact benefit to their employee pool. Combined with employer-matched round-ups, Milo can be extremely impactful in comparison to other currently offered benefits. We’re excited about our employer benefit platform going forward.

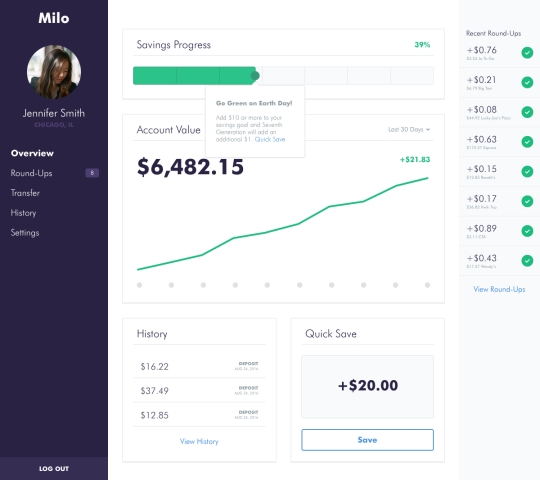

The Milo interface

The Milo interface

Why Milo and not one of the other savings apps?

While the general mechanics of how we are saving – via rounding up purchases to the next highest dollar – aren’t exclusive to Milo, the ways in which we are engaging with the community, the merchants in our Milo Marketplace and employers offering Milo as an employee benefit allow users to optimize the value and financial return on their savings.

What’s been the biggest challenge so far?

The biggest challenge has been making sure that all the safeguards and security are in place and rock-solid so that our users have peace of mind that their hard-earned savings are safe with Milo. As we are handling consumer funds, we’ve needed to not only insure that our application is safe-guarded, but that all of our processes are compliant with financial regulations and that all the funds held with Milo are FDIC insured. We take this very seriously.

Are there unique challenges or opportunities to doing a startup in greater Milwaukee?

There has been a lot written about Wisconsin and Milwaukee not being "startup friendly." We haven’t run into any challenges or roadblocks as of yet. I really feel that if you build a business that offers significant value to your customer, where that business was started shouldn’t be a show-stopper. There’s quite a bit of energy in the MKE/Madison startup community that we feel is important to fostering young companies like ours. Two members of our founding team (Justin Seidl and Rob Schwartz) are in Chicago, and we feel that Milo benefits from the vibrancy of that startup community as well. In terms of raising our initial round of funds, we are certainly hopeful that we are supported by the Wisconsin investment community, although we haven’t seen many FinTech investments in Wisconsin to this point.

What else do we need to know about Milo?

Well, for one, I’m extremely proud of the team we’ve put together. We’ve got extremely talented founders leading both the business and development and design of the Milo platform. As a founder, you can have the best idea since sliced bread, but without the team in place to execute the vision, you really have nothing.

Secondly, we’re launching Milo in November, just in time for the holidays, so we’d love everyone here in Southeast Wisconsin to start saving with us and engage with us – and ask their employers to offer Milo, as well.

Define success.

Success to me will be building a large, engaged community of Milo users and marketplace and employer partners, making an impact on their lives and then using our success to give back to our community. We really are excited that we can truly help people with what we are doing and "Make Change Happen."

The founders of Milo Savings

The founders of Milo Savings

A life-long and passionate community leader and Milwaukeean, Jeff Sherman is a co-founder of OnMilwaukee.

He grew up in Wauwatosa and graduated from Marquette University, as a Warrior. He holds an MBA from Cardinal Stritch University, and is the founding president of Young Professionals of Milwaukee (YPM)/Fuel Milwaukee.

Early in his career, Sherman was one of youngest members of the Greater Milwaukee Committee, and currently is involved in numerous civic and community groups - including board positions at The Wisconsin Center District, Wisconsin Club and Marcus Center for the Performing Arts. He's honored to have been named to The Business Journal's "30 under 30" and Milwaukee Magazine's "35 under 35" lists.

He owns a condo in Downtown and lives in greater Milwaukee with his wife Stephanie, his son, Jake, and daughter Pierce. He's a political, music, sports and news junkie and thinks, for what it's worth, that all new movies should be released in theaters, on demand, online and on DVD simultaneously.

He also thinks you should read OnMilwaukee each and every day.